How Balance Billing Buries Marketplace Plan Holders Financially?

Analysis reveals 9 key thematic connections.

Key Findings

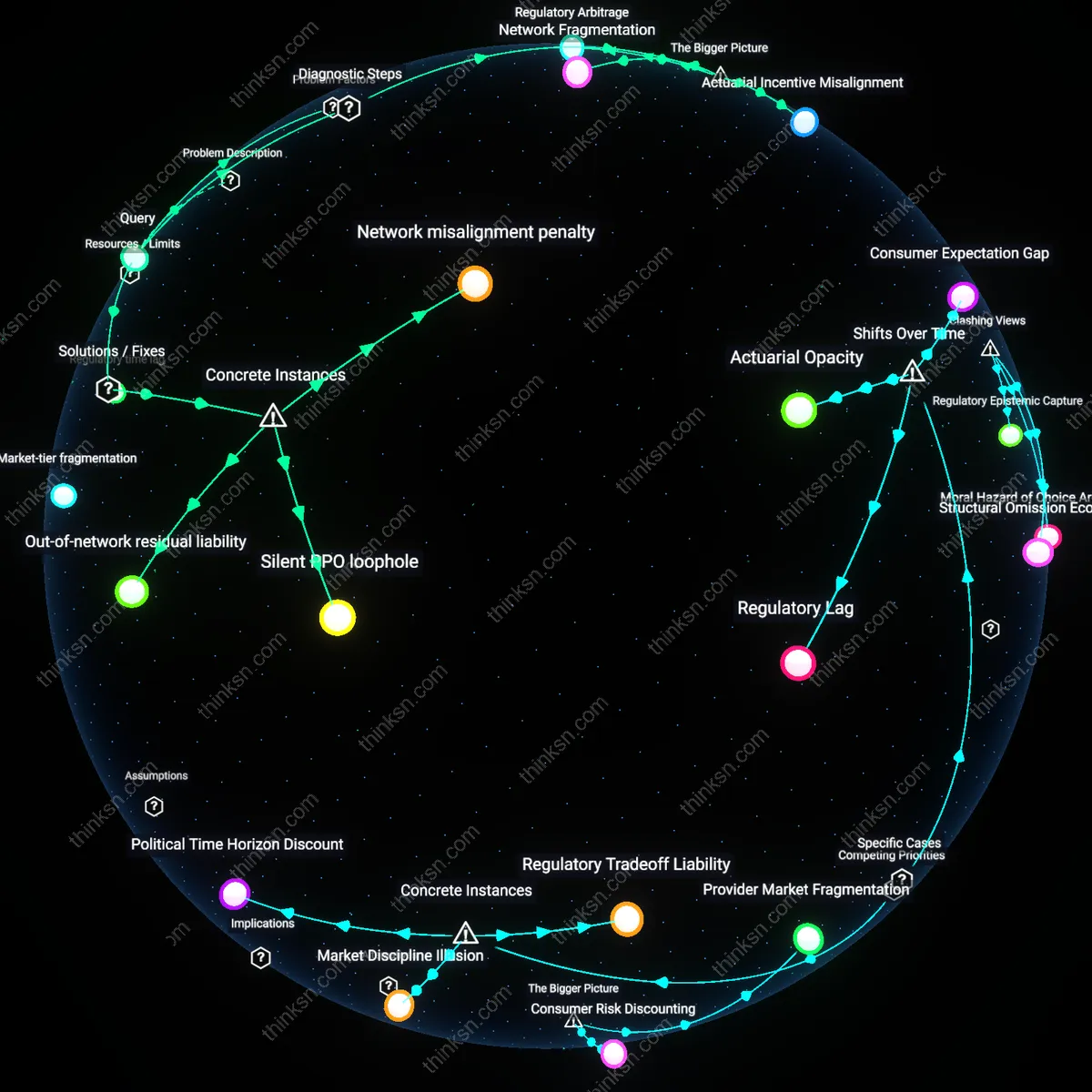

Market-tier fragmentation

The shift from employer-based to marketplace-driven health insurance after the Affordable Care Act created a segmented provider network structure where narrow networks became the norm, disproportionately exposing enrollees to out-of-network care because lower-premium plans deliberately excluded high-cost specialists and facilities to maintain affordability — a design trade-off obscured at enrollment. This fragmentation intensified over time as insurers optimized for actuarial efficiency rather than continuity of access, normalizing balance billing in emergency and referral contexts where network adequacy was misaligned with patient care pathways.

Regulatory time lag

Between the mid-2000s and the 2016–2022 expansion of individual market plans, federal and state balance billing regulations lagged behind changes in insurance distribution models, allowing legacy enforcement mechanisms — calibrated to employer-sponsored insurance — to fail in protecting patients during unanticipated out-of-network encounters, especially in independent practice settings. The non-obvious consequence was not simple loophole exploitation but the institutionalization of billing uncertainty as a systemic feature, rather than a flaw, because protections evolved incrementally while provider-contracting practices changed discretely and asymmetrically.

Asymmetric risk normalization

Prior to 2010, balance billing was rare outside of elective care due to broad-network indemnity plans dominant in the commercial market, but the post-ACA era’s emphasis on cost-sensitive insurance designs incentivized high-deductible, narrow-network products that redefined unexpected out-of-pocket exposure as a manageable norm rather than an anomaly, embedding financial unpredictability into patient planning through deliberate risk transfer mechanisms. The shift was not merely technical but ideological — normalizing volatility in care costs as a shared responsibility, which made legislative and public resistance to its harms politically attenuated despite rising financial distress.

Network Fragmentation

Marketplace plans enroll patients in narrow networks that exclude many established providers, increasing reliance on out-of-network care during emergencies or specialty treatment, where balance billing remains legal and unregulated; this structural exclusion is amplified by insurers' cost-containment strategies and providers' independent contracting decisions, creating systemic exposure for patients who cannot predict or avoid these gaps. The non-obvious consequence is that even compliant patients—those who follow plan guidelines—are funneled into balance billing scenarios not through personal error but institutional misalignment between insurance design and actual care ecosystems.

Regulatory Arbitrage

States lacking comprehensive balance billing protections allow providers to exploit gaps in federal shielding—such as the No Surprises Act’s limitations on emergency care but weaker oversight in air ambulance or facility billing—enabling targeted financial extraction from marketplace enrollees who are more likely to use high-turnover, cost-sensitive plans with less advocacy infrastructure; this occurs because state-federal regulatory misalignment creates legal loopholes that providers with profit-maximizing incentives can weaponize. The underappreciated dynamic is that federal preemption does not override all state weaknesses, allowing financially distressed hospitals in loosely regulated markets to disproportionately target privately insured, non-Medicare patients.

Actuarial Incentive Misalignment

Insurers offering marketplace plans maximize profits by minimizing premium costs through narrow provider contracts and high deductibles, which inadvertently encourage provider-side revenue defense via balance billing when payments are deemed insufficient, particularly in unregulated specialties like anesthesiology or radiology; because insurers price plans assuming stable out-of-pocket risk, they do not internalize the indirect financial harm from provider opportunism fueled by underreimbursement. The overlooked mechanism is that the ACA’s risk-adjustment system fails to penalize plans whose network design provokes downstream balance billing, leaving patients as collateral in a silent actuarial negotiation between payers and providers.

Network misalignment penalty

State-based marketplace plans in Texas disproportionately expose patients to balance billing because insurers and providers often operate under divergent network definitions due to lack of centralized oversight, as seen in the 2021 Baylor Scott & White Health disputes where patients enrolled in Silver-level marketplace plans were billed unexpectedly for out-of-network emergency care despite plan marketing suggesting full in-network coverage; this misalignment persists because marketplace certification focuses on premium eligibility rather than network accuracy, revealing that patients bear financial risk not from individual choices but from structural discoordination between plan design and provider contracting.

Silent PPO loophole

Patients in Colorado's marketplace are vulnerable to balance billing due to silent PPO arrangements, where providers are contracted with insurers without patient or provider awareness—exemplified by a 2019 case at Centura Health where emergency room patients received bills from unaffiliated anesthesiologists who leveraged silent PPO clauses to bypass in-network requirements; because insurers do not disclose these shadow contracts and providers are unaware of their de facto network status, patients cannot anticipate cost exposure, demonstrating that the lack of transparency in intermediary agreements enables third-party providers to exploit reimbursement ambiguities for secondary billing.

Out-of-network residual liability

In New York, despite comprehensive balance billing protections for emergency services post-2014, patients with marketplace plans on Essential Plan 111 still face residual liability through behavioral health carve-outs, as demonstrated by a 2022 lawsuit involving Northwell Health’s outpatient psychiatry services where patients were balance billed because the state’s shield law exempted non-emergency specialty services when delivered by unaffiliated network providers; this exception persists because federal marketplace regulations allow state waivers to exclude mental health parity enforcement, exposing a gap where statutory protections are systematically undercut by modular benefit design.