Inflation Spikes: Commodities Tilt or Patience?

Analysis reveals 6 key thematic connections.

Key Findings

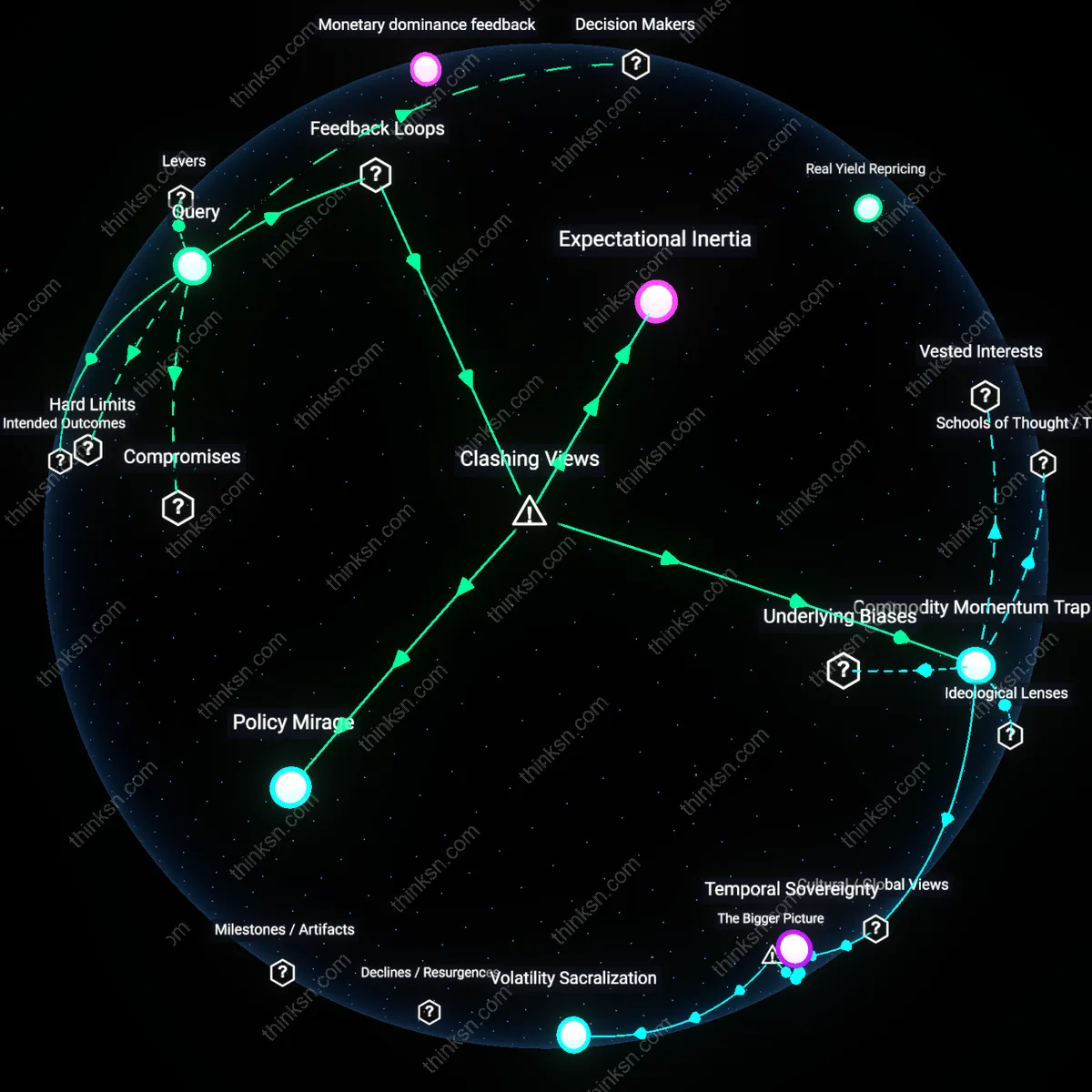

Expectational Inertia

Investors should maintain patience during temporary inflation spikes because financial-market pricing, particularly in long-dated inflation swaps and Treasury inflation-protected securities, reflects a regime of anchored expectations that dampens speculative momentum into commodities. Central banks, especially the Federal Reserve and ECB, have established credibility through consistent forward guidance and policy tightening, creating a balancing feedback loop where rising commodity positions trigger mean-reverting flows as institutions arbitrage perceived deviations from inflation targets. This dynamic is non-obvious because market commentary typically overreacts to near-term CPI prints, ignoring how dealer positioning in inflation derivatives reinforces stability rather than runaway inflation fears.

Commodity Momentum Trap

Investors should tactically shift to commodities during temporary inflation spikes because the collective rewiring of risk allocation models in pension funds and endowments now incorporates trend-following overlays that amplify initial commodity moves into self-reinforcing rallies, even amid stable long-term inflation expectations. Mechanisms like CTAs (Commodity Trading Advisors) deploying momentum strategies reweight portfolios based on short-term price breaks, creating a reinforcing feedback loop that detaches commodity returns from monetary policy signals. This contradicts the standard view that anchored expectations imply passive holding, revealing instead how technical actors exploit brief windows of price instability despite macro consensus.

Policy Mirage

Investors should maintain patience not due to expectation anchoring but because central bank credibility is a retrospective narrative constructed only after stabilization, meaning that during active inflation spikes, delayed policy response creates a perceptual lag in which commodities appear mispriced when they are actually signaling real supply-chain imbalances. The balancing loop emerges not from market discipline but from the time-bound failure of policymakers to act pre-emptively, allowing physical scarcity dynamics in energy or agriculture to transiently decouple from financialized inflation bets. This challenges the dominant view by showing that patience is rewarded not because expectations are anchored, but because the illusion of control delays necessary tactical shifts until it's too late.

Expectations arbitrage

Investors should maintain patience during temporary inflation spikes with anchored expectations because financial markets already price in duration-contingent risk, and tactical commodity shifts incur frictional costs that erode returns when mean reversion occurs within central bank credibility windows. Traders, algorithmic systems, and institutional portfolios interact under the assumption that policy credibility constrains inflation duration, making commodity overweights a negative-sum signal-to-noise exploit; the non-obvious insight is that the real arbitrage lies not in asset class timing but in the wedge between realized volatility and expected persistence—where position churn becomes the hidden tax.

Supply network reflex

Investors should tactically shift to commodities during temporary inflation spikes because primary sector input bottlenecks trigger nonlinear repricing in mid-cycle industrial chains, and these distortions propagate faster than monetary policy transmission, creating short-term optionality in physical-linked derivatives. Mining firms, freight operators, and inventory financiers amplify price signals through forward contracting behaviors that lock in margin compression or expansion before CPI peaks, meaning patient investors systematically miss the inflection in cash flow rerouting; the overlooked mechanism is that commodity markets act as leading sensors of input scarcity, not just inflation proxies.

Monetary dominance feedback

Investors should maintain patience because the anchoring of inflation expectations reflects a regime of monetary dominance where central bank balance sheet credibility suppresses the pass-through from transitory shocks to wage-price spirals, thereby limiting commodity demand elasticity and capping roll yields in futures curves. Treasury markets, inflation swap dealers, and pension hedgers continually validate this regime through breakeven volatility compression, which systematically penalizes momentum-based commodity entries post-spikes; the underappreciated dynamic is that monetary credibility functions as a structural dampener, transforming apparent tactical opportunities into mean-reverting noise.