When Does Active Management Cost More Than It Saves?

Analysis reveals 9 key thematic connections.

Key Findings

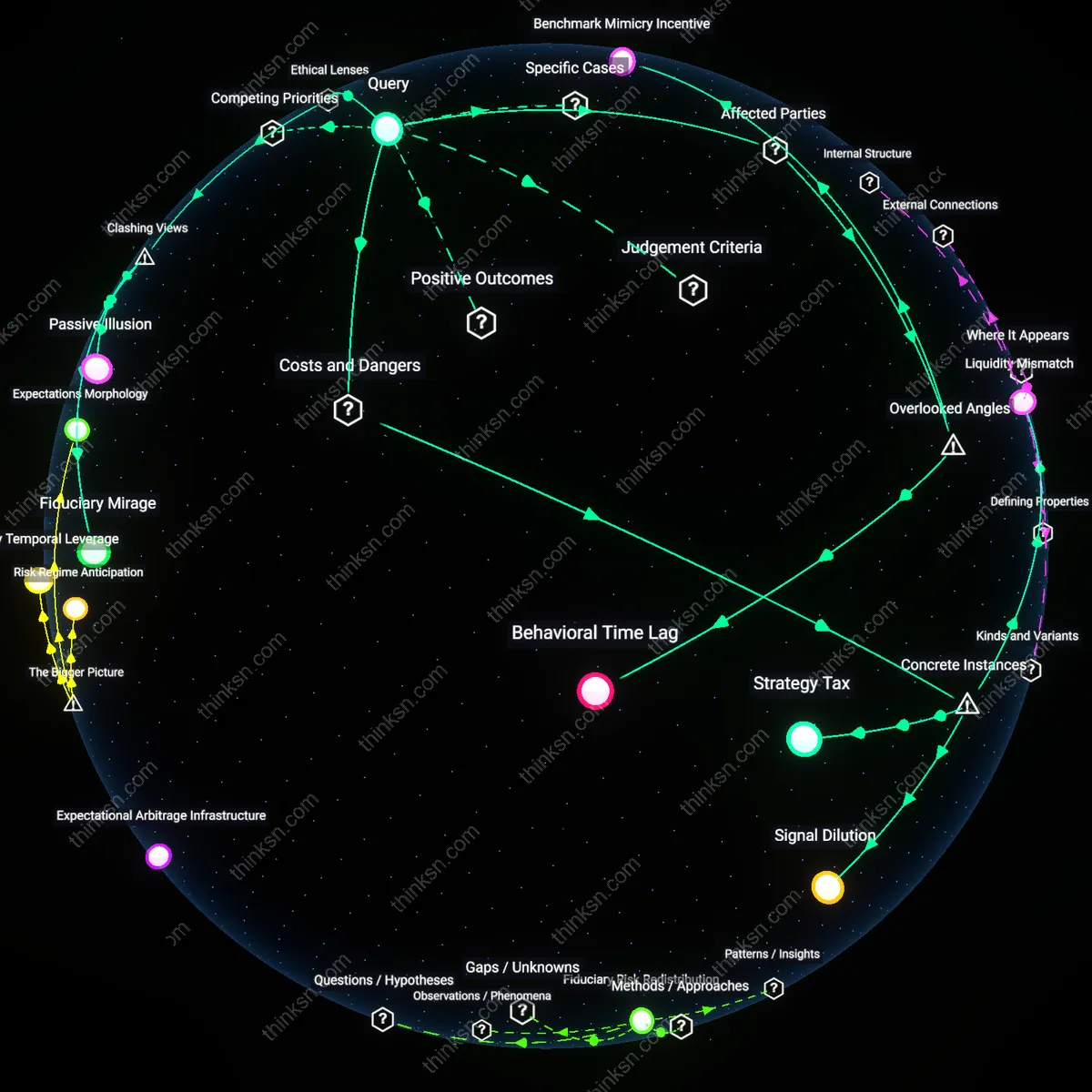

Behavioral Time Lag

Retail investors transitioning from passive to active bond funds during Fed tightening cycles face delayed responsiveness in manager decision-making, amplifying volatility exposure. Portfolio managers dependent on quarterly rebalancing and backward-looking macro indicators routinely lag real-time yield shifts, leaving retail investors—particularly near-retirement cohorts in 401(k) plans—locked in underperforming allocations for months after inflection points. This overlooked temporal friction between investor action and manager reaction means the cost of active management is not just in fees, but in embedded inertia that passive strategies inherently avoid, reshaping the traditional cost-benefit analysis around timing risk rather than expense ratios.

Regulatory Arbitrage Gap

Active managers exploiting regulatory exemptions under SEC Rule 2a-7 to hold illiquid derivatives in 'duration-hedged' portfolios systematically increase tail risk during rate volatilities, disproportionately affecting municipal pension boards relying on AAA-rated fund labels. These funds often mask concentration in off-balance-sheet swaptions that decay unpredictably under rapid yield curve shifts, a dynamic hidden from standard risk metrics like duration or convexity. The overlooked mechanism is not fund performance per se, but the regulation-induced incentive for managers to stretch for yield in opaque instruments—costs that only crystallize in crises, skewing long-term outcomes against passive index exposure despite apparent short-term stability.

Benchmark Mimicry Incentive

EM bond portfolio managers employed by multilateral development banks face compensation-linked benchmarks that incentivize passive-like tracking even when mandate allows active discretion, resulting in higher fees without meaningful volatility buffering during sovereign yield shocks. Because their performance is evaluated against a synthetic index that includes non-tradable securities, they are structurally prevented from effective reallocation, creating a perverse dynamic where investors pay for active management but receive a lagged, fee-inflated version of passive exposure. This hidden misalignment between incentive structure and operational reality renders active management more costly than passive not due to underperformance, but due to paid redundancy—an often-invisible tax on institutional mandates.

Strategy Tax

Active management fees outweigh benefits when duration bets misalign with regime shifts, as seen in the 2022 collapse of UK Liability-Driven Investment (LDI) funds, where rapid interest rate hikes exposed leveraged hedge shortfalls, forcing the Bank of England to intervene; the actual cost was not just underperformance but structural fragility introduced by active duration overlays atop passive mandates, revealing that active interventions can convert market risk into systemic risk under stress.

Signal Dilution

In 2013, PIMCO’s Total Return Fund—led by Bill Gross—began deteriorating after key personnel changes and inconsistent interest rate positioning, leading to massive outflows and underperformance versus the Bloomberg Aggregate Index; this episode demonstrates that the informational edge claimed by active managers can degrade imperceptibly due to internal organizational drift, turning management costs into a drag without investors realizing the strategy has lost coherence until performance collapses.

Liquidity Mismatch

During the March 2020 ‘dash for cash,’ actively managed bond ETFs like the iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD) saw widening spreads and price dislocations despite passive benchmarks holding value, because active portfolio managers faced redemption pressure and had to sell liquid bonds first, distorting returns; this reveals that active management introduces endogenous liquidity risk in fixed income strategies during volatility spikes, where the act of managing becomes a source of performance degradation rather than mitigation.

Fiduciary Mirage

Active management’s costs exceed its benefits when fund managers exploit asymmetric information to justify fees, not outperformance—positioning themselves as stewards under fiduciary duty while operating through legal loopholes in the Investment Advisers Act of 1940 that permit fee structures decoupled from risk-adjusted returns; this dynamic reveals how ethical obligations codified under deontological trust doctrines are systematically hollowed out by performative compliance in asset management, making the fiduciary commitment a ritual rather than a constraint.

Volatility Rent

Active management becomes disadvantageous when institutional investors in G7 bond markets internalize macroeconomic noise as tradable risk, allowing asset managers to monetize interest rate volatility itself through frequent rebalancing—framed as prudential risk mitigation under utilitarian portfolio theory, but in practice functioning as a rent-extraction mechanism enabled by the Federal Reserve’s post-2008 forward guidance regime; this exposes how the ethical justification for discretion (maximizing outcomes across market cycles) morphs into a structural subsidy for intermediaries during periods of policy-induced uncertainty.

Passive Illusion

The costs of active management exceed their benefits when passive investors relying on ETFs tracking aggregate bond indices unknowingly concentrate systemic risk through liquidity mirroring, creating ethical externality under Rawlsian fairness principles—where the ostensibly neutral market mechanism of indexation, protected by deregulatory ideologies like those in the SEC’s Regulation NMS, enables free-riding on price discovery performed by active traders; this renders the passive choice not a benign default but a politically enabled defection from collective market functioning, destabilizing the very neutrality it presumes.